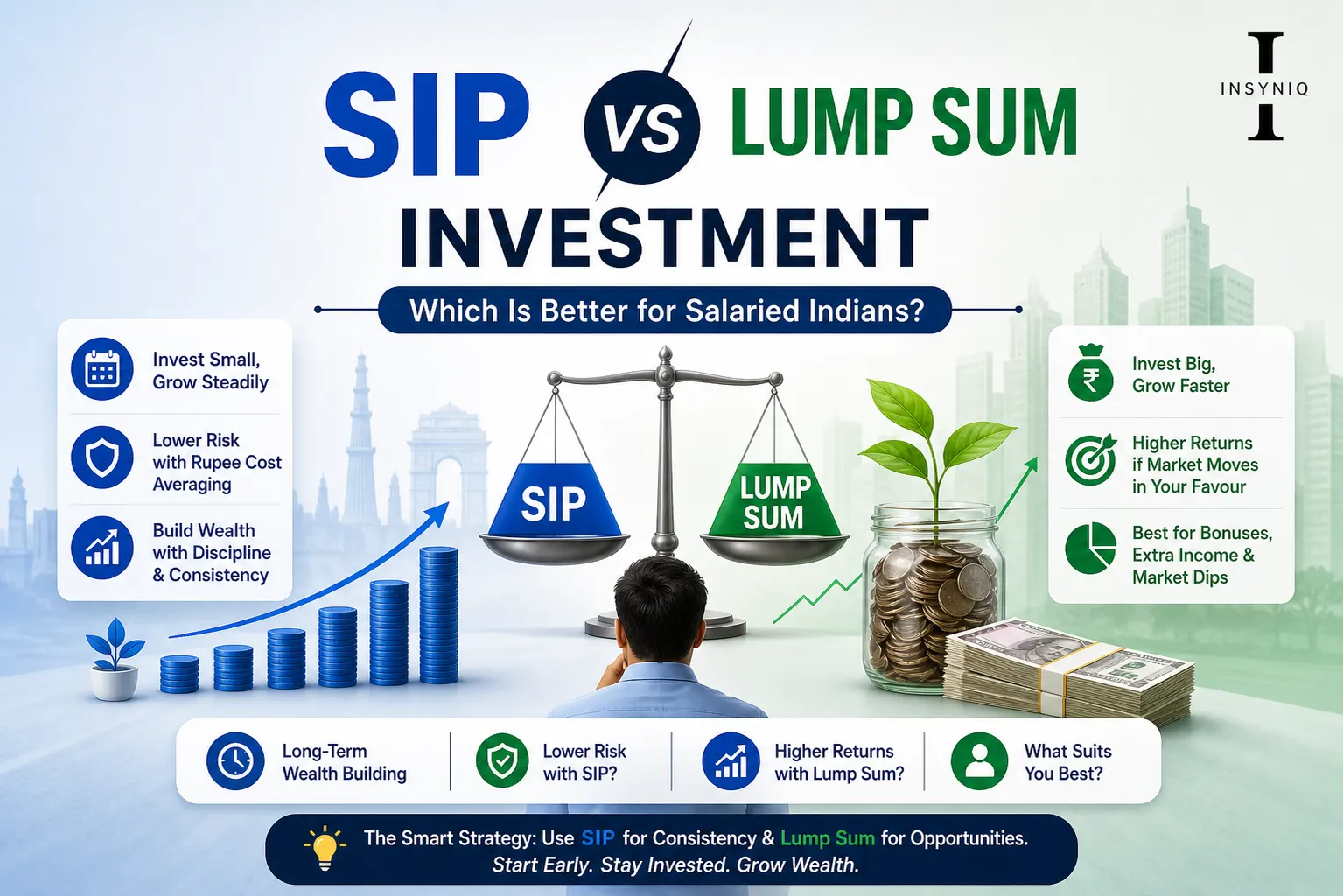

Quick Answer: SIP vs Lump Sum Investment:

- SIP: invests a fixed amount every month automatically, ideal for salaried individuals

- Lump Sum: invest a large amount all at once, ideal when markets are low

- SIP reduces risk through rupee cost averaging; you buy more units when prices fall

- Lump Sum gives higher returns if timed correctly during market dips

- For most salaried Indians earning ₹25,000–₹80,000/month, SIP is the safer and smarter choice

- Minimum SIP amount starts from just ₹100/month on platforms like Groww and Zerodha

- Both methods invest in the same mutual funds; only the timing of investment differs

- Tax benefit: ELSS mutual funds through SIP qualify for Section 80C deduction up to ₹1.5 lakh per year

- Best of both worlds: start a SIP monthly and invest a lump sum whenever you receive a bonus or incentive

If you are a salaried professional in India, you have probably heard two pieces of advice that seem to contradict each other. One person says start a SIP immediately. Another says wait for the market to fall and invest a lump sum. Both sound reasonable, but which one is actually right for someone earning a monthly salary?

The honest answer depends on your income, your financial goals, and your risk tolerance. This guide breaks down SIP and lump sum investment completely how each works, which gives better returns, and which one makes more sense for your specific situation in 2026.

What Is a SIP (Systematic Investment Plan)?

A SIP or Systematic Investment Plan is a method of investing a fixed amount of money into a mutual fund at regular intervals, usually every month. Instead of investing all your money at once, you invest small amounts consistently over time, which reduces risk and builds wealth steadily.

A SIP works like a recurring deposit, but instead of a bank account, your money goes into a mutual fund. Every month on a fixed date, say the 5th or 10th, a predetermined amount is automatically debited from your bank account and invested into your chosen mutual fund.

For example, if you start a SIP of ₹5,000 per month in a Nifty 50 index fund, your bank automatically transfers ₹5,000 every month into that fund. Over 10 years that is ₹6,00,000 invested but because of market growth and compounding, the actual value of your investment at historical average returns of 12% per year would be approximately ₹11,61,695.

The power of SIP is not just discipline it is something called rupee cost averaging, which we will explain in detail shortly.

What Is a Lump Sum Investment?

A lump sum investment means investing a large amount of money into a mutual fund or stock all at once in a single transaction. Unlike SIP where you invest monthly, lump sum investing means your entire capital enters the market on one specific day.

For example, if you receive a Diwali bonus of ₹1,00,000 and invest the entire amount into a mutual fund in one transaction, that is a lump sum investment.

The advantage of a lump sum is that if the market rises after your investment, your entire capital benefits from that growth. The disadvantage is that if the market falls right after you invest, your entire capital loses value immediately unlike SIP where only that month’s instalment is affected.

What Is Rupee Cost Averaging and Why Does It Matter?

Rupee cost averaging is the biggest advantage of SIP investing and the main reason financial advisors recommend it for salaried Indians.

Here is how it works with a simple example:

Imagine you invest ₹5,000 every month in a mutual fund. The price of one unit of that fund changes every month based on the market:

| Month | Unit Price | Units Purchased |

|---|---|---|

| January | ₹100 | 50 units |

| February | ₹80 | 62.5 units |

| March | ₹60 | 83.3 units |

| April | ₹80 | 62.5 units |

| May | ₹100 | 50 units |

Total invested: ₹25,000 Total units purchased: 308.3 units Average cost per unit: ₹81.08

If you had invested ₹25,000 as a lump sum in January at ₹100 per unit, you would have only 250 units at the same cost.

With SIP you ended up with 308 units versus 250 units for the same ₹25,000 because you automatically bought more units when prices were lower. This is rupee cost averaging and it is why SIP consistently outperforms lump sum for investors who cannot predict market movements.

SIP vs Lump Sum ( Comparison )

Which Gives Better Returns?

A lump sum investment gives better returns than SIP IF you invest during a market low and the market rises significantly afterwards. However, SIP gives more consistent and safer returns over long periods because it averages out market volatility through rupee cost averaging. For most investors who cannot time the market, SIP outperforms lump sum over 10+ year periods.

Research by AMFI India shows that a SIP of ₹10,000 per month in Nifty 50 index funds over 15 years (2009–2024) generated average annual returns of 13.2%, turning ₹18,00,000 of total investment into approximately ₹52,00,000. A lump sum of the same ₹18,00,000 invested in 2009 would have grown to approximately ₹67,00,000 at the same 13.2% annual return but only because 2009 was a market low after the 2008 crash. Most investors do not have that perfect timing.

Which has a lower risk?

SIP has a significantly lower risk than lump sum investing because your money enters the market gradually over time rather than all at once. If the market falls after a lump sum investment, you lose your entire capital. With SIP, only that month’s instalment is affected by a market fall.

For a salaried Indian who invests monthly from their salary, SIP is the natural choice it aligns perfectly with when you receive money. You do not need to wait and accumulate a large amount before starting. You can begin with as little as ₹500 per month and increase the amount as your salary grows.

Which Is Better for a Salaried Person Earning ₹30,000–₹60,000 Per Month?

Direct Answer (PAA): SIP is better for salaried Indians earning ₹30,000 to ₹60,000 per month. At this income level, saving a large lump sum is difficult and investing monthly from salary is more practical. SIP also enforces financial discipline by automating investments before you can spend the money.

At ₹30,000 salary, even a SIP of ₹3,000 per month (10% of salary) invested in a Nifty 50 index fund for 20 years at 12% annual returns grows to approximately ₹29,98,519 nearly ₹30 lakhs from just ₹3,000 per month.

The key insight is this: you do not need a large amount to start building serious wealth. You need consistency and time.

When Is a Lump Sum Investment Better Than SIP?

Despite SIP being better for most salaried Indians, there are specific situations where lump sum investment makes more sense:

When markets have fallen significantly, if the Sensex or Nifty has fallen 20–30% from its peak, investing a lump sum captures the recovery upside for your entire capital. This is called “buying the dip” and it is the one scenario where a lump sum clearly wins.

When you receive a large one-time amount; annual bonus, gratuity payment, inheritance, or proceeds from selling property. In these situations, you have a large amount available that you would not have through monthly savings. Investing it as a lump sum makes sense rather than letting it sit in a savings account earning 3–4% interest.

When investing in debt mutual funds; for debt funds which are lower-risk and less volatile, lump sum investment works well because the returns are more predictable and market timing matters less.

When your investment horizon is very long; if you are investing for 20–30 years, the impact of market volatility at the entry point becomes less significant over such a long time horizon.

The Smart Strategy for Salaried Indians

The most effective strategy for a salaried Indian is not choosing between SIP and lump sum, it is using both intelligently:

Step 1: Start a monthly SIP from your salary immediately even ₹500 to ₹1,000 to begin. Automate it so it happens without any action from you every month.

Step 2: Every time you receive extra money, an annual bonus, incentive, tax refund, freelance income invest it as a lump sum in the same fund or a different one.

Step 3: Increase your SIP amount by 10% every year as your salary grows. This is called a Step-Up SIP and most platforms offer this feature for free.

This combined approach gives you the consistency of SIP and the return-maximising potential of lump sum whenever you have extra funds available.

Best Mutual Funds for SIP in India in 2026

For a beginner salaried investor, these categories of mutual funds work best for SIP:

For long-term wealth building (10+ years): Nifty 50 index funds are low-cost, tracks India’s top 50 companies, historically had 12–13% annual returns. Examples: UTI Nifty 50 Index Fund, HDFC Nifty 50 Index Fund.

For tax saving (ELSS Section 80C benefit): Equity Linked Savings Scheme funds 3-year lock-in period, tax deduction up to ₹1.5 lakh per year under Section 80C. Examples: Mirae Asset ELSS Tax Saver, Quant ELSS Tax Saver.

For balanced risk (Flexi Cap funds): Funds that invest across large, mid, and small-cap companies. Examples: Parag Parikh Flexi Cap Fund, HDFC Flexi Cap Fund.

For conservative investors: Hybrid or balanced advantage funds that automatically shift between equity and debt based on market conditions. Lower returns than pure equity but significantly lower risk.

How to Start a SIP in India Step by Step

To start a SIP in India you first need a Demat and trading account with a broker like Groww or Zerodha. If you have not opened one yet, read our complete guide on how to open a Demat account in India before continuing.

Once your account is active:

Step 1: Log in to your Groww or Zerodha account and go to the Mutual Funds section.

Step 2: Search for the fund you want to invest in, for example “UTI Nifty 50 Index Fund.”

Step 3: Click “Start SIP” → enter the monthly amount → select the SIP date (choose a date 2–3 days after your salary credit date).

Step 4: Set up auto-pay from your bank account. Your bank will automatically debit the SIP amount every month.

Step 5: Click Confirm. Your first SIP instalment will be invested on your chosen date.

The entire process takes under 10 minutes and your investment runs automatically every month from that point.

You can use the free SIP calculator on Groww to calculate exactly how much your investment will grow over time at different return rates.

SIP vs Lump Sum ( Tax Implications )

Both SIP and lump sum investments in equity mutual funds are taxed the same way in India:

Short Term Capital Gains (STCG): if you sell your mutual fund units within 1 year of purchase, gains are taxed at 20% (revised in Budget 2024).

Long Term Capital Gains (LTCG): if you hold for more than 1 year, gains above ₹1.25 lakh per year are taxed at 12.5% without indexation benefit (revised in Budget 2024).

Important note for SIP investors: Each monthly SIP instalment is treated as a separate investment with its own purchase date. So when you sell your SIP units, some may qualify for LTCG and some for STCG depending on how long each specific instalment has been held.

Tax saving tip: Invest in ELSS mutual funds through SIP to get a deduction of up to ₹1.5 lakh per year under Section 80C of the Income Tax Act, reducing your taxable income directly.

Always consult a SEBI-registered financial advisor or a chartered accountant for personalised tax advice based on your specific income and investment situation.

Is SIP better than FD (Fixed Deposit) for salaried employees?

For long-term goals of 5 years or more, SIP in equity mutual funds typically gives 3 to 4 times better returns than FD. FD rates in India in 2026 average 6.5–7.5% per year while equity mutual fund SIPs have historically delivered 11–14% per year over long periods. However FD is safer and guaranteed SIP returns are market-linked and not guaranteed.

SIP is better than FD for goals that are 7+ years away such as retirement, children’s education, or buying a house. For short-term goals of 1–3 years or for an emergency fund, FD is safer and more appropriate. The ideal approach is to maintain 3–6 months of expenses in an FD as an emergency fund and invest everything beyond that in SIP for long-term wealth building.

Can I stop my SIP anytime in India?

Yes, you can pause or stop your SIP anytime without any penalty. Log in to your broker platform, go to your active SIPs, and click Stop or Pause. Your already-invested units remain in your account and continue to grow only future instalments are stopped.

There is no lock-in period for most SIP investments in equity mutual funds except ELSS funds which have a mandatory 3-year lock-in from each instalment date. Stopping a SIP does not mean you lose your invested money it simply stops future automatic investments. You can restart the SIP at any time with the same or a different amount.

What happens to my SIP if the market crashes?

If the market crashes while your SIP is running, your existing units lose value temporarily but your upcoming SIP instalments buy more units at the lower price. This is rupee cost averaging working in your favour. A market crash is actually beneficial for active SIP investors because they accumulate more units at lower prices.

The biggest mistake investors make during a market crash is stopping their SIP out of fear. This is exactly the wrong move, it locks in your losses and you miss buying cheaper units during the recovery. Historical data from AMFI India shows that investors who continued SIPs through the 2008 crash, 2020 COVID crash, and 2022 correction all recovered and gained significantly within 2–3 years compared to those who stopped.

How much should I invest in SIP every month as a beginner?

Start with 10–15% of your monthly take-home salary as a SIP amount. If you earn ₹30,000 per month, start with ₹3,000 to ₹4,500 per month. If you earn ₹50,000, start with ₹5,000 to ₹7,500. Increase the amount by 10% every year as your salary grows.

The most important principle is to start immediately with whatever amount you can afford rather than waiting until you can invest a “significant” amount. A SIP of ₹500 per month started today is worth more than a SIP of ₹5,000 planned for next year because compounding rewards time above everything else. Set up the SIP for the day after your salary gets credited so the money is invested before you can spend it.

Is a lump sum or SIP better during a bull market?

Direct Answer: During a bull market where prices are rising continuously, SIP slightly underperforms a lump sum because you keep buying at higher and higher prices each month. In a pure bull market, investing the entire amount as a lump sum at the start would give better returns. However, since no one can predict how long a bull market will last, SIP remains the safer choice for most investors.

The challenge with trying to use a lump sum during a bull market is knowing when the bull market will end. Many investors who invested large lump sums in January 2008 (bull market peak) lost 50–60% of their value by March 2009. SIP investors during the same period recovered much faster because they kept buying cheaper units throughout the crash. This is why most financial advisors recommend SIP regardless of market conditions for retail investors.

Frequently Asked Questions

Q1: What is the minimum amount to start a SIP in India?

The minimum SIP amount in India starts from just ₹100 per month on platforms like Groww, Zerodha, and Paytm Money. Most mutual funds have a minimum SIP of ₹500 per month.

There is genuinely no excuse to delay starting a SIP because of insufficient funds. Even ₹500 per month invested consistently in a Nifty 50 index fund for 25 years at 12% annual returns grows to approximately ₹9.4 lakhs from just ₹1.5 lakhs of total investment. The power is entirely in starting early and staying consistent not in the amount.

Q2: Can I have multiple SIPs at the same time?

Yes, you can run multiple SIPs simultaneously in different mutual funds. There is no restriction on how many SIPs you can have at one time.

Running multiple SIPs is actually recommended for diversification. A common beginner strategy is to split your monthly SIP amount across two or three funds for example 60% in a Nifty 50 index fund, 30% in a mid-cap fund, and 10% in an ELSS fund for tax saving. This spreads your risk across different market segments while keeping your investment automated and disciplined.

Q3: Is SIP and mutual funds the same thing?

No, SIP is a method of investing, not an investment itself. A mutual fund is the actual investment product. SIP is simply the process of investing into a mutual fund in regular monthly instalments instead of all at once.

Think of it this way: a mutual fund is the destination and SIP is how you get there in small regular steps instead of one big jump. You can invest in the same mutual fund through both SIP (monthly) and lump sum (one-time) the fund itself is identical. Many investors do both, a monthly SIP plus occasional lump sum top-ups when they have extra money.

Q4: What is a Step-Up SIP and should I use it?

A Step-Up SIP automatically increases your SIP amount by a fixed percentage every year usually 10%. If you start a SIP of ₹5,000 per month with a 10% annual step-up, it becomes ₹5,500 next year, ₹6,050 the year after, and so on. This is highly recommended for salaried investors whose income grows each year.

The impact of step-up is dramatic. A regular SIP of ₹5,000 for 20 years at 12% returns grows to approximately ₹49.96 lakhs. The same SIP with a 10% annual step-up grows to approximately ₹1.05 crore more than double for the same 12% returns. Most platforms including Groww and Zerodha offer step-up SIP as a free feature when setting up your investment.

Q5: How do I choose between SIP and lump sum if I just received my annual bonus?

If you received a bonus and the market has not fallen recently, split it, invest 50% as a lump sum immediately and spread the remaining 50% over 6 months as a systematic transfer plan (STP) from a liquid fund into your equity fund.

This hybrid approach gives you the benefit of putting a significant amount to work immediately while still protecting 50% of your capital through gradual market entry. First, check where the Nifty 50 is relative to its 52-week high. If it is within 5% of its all-time high, the STP approach for the full amount is safer. If it has already corrected 15–20% from its peak, investing the full lump sum makes more sense as you are buying at a relative discount.

Q6: Are SIP returns guaranteed in India?

No, SIP returns in equity mutual funds are not guaranteed. They are market-linked, which means returns depend on how the stock market performs. Historical average returns of Nifty 50 index funds have been 11–13% per year over 10+ year periods, but past returns do not guarantee future performance.

This is the fundamental difference between SIP in mutual funds and a fixed deposit or PPF, FD and PPF offer guaranteed returns (currently 6.5–7.5% and 7.1% respectively) while SIP returns are variable. However, over long periods of 10 years or more, equity mutual fund SIPs have historically beaten FD, PPF, and inflation by a significant margin. The key is staying invested through market cycles and not withdrawing during temporary downturns.

Q7: Can NRIs invest in SIP in India?

Yes, NRIs (Non-Resident Indians) can invest in SIP in India through an NRE or NRO bank account. They need to complete KYC with their Indian broker using their passport and overseas address proof.

NRIs from most countries can invest in Indian mutual funds through SIP. However, NRIs from the USA and Canada face additional compliance requirements due to FATCA regulations, which means some Indian fund houses do not accept investments from US and Canada-based NRIs. NRIs should confirm with their chosen broker whether their country of residence is supported before completing the account setup.

Q8: What is the difference between SIP in mutual funds and a recurring deposit (RD)?

Both SIP and RD involve investing a fixed amount every month, but SIP invests in market-linked mutual funds while RD deposits money in a bank at a fixed interest rate. RD is safer with guaranteed returns of around 6–7% while SIP has variable returns historically averaging 11–13% over long periods.

Choose RD for short-term goals of 1–3 years where you cannot afford any loss of capital like saving for a wedding, travel, or emergency fund. Choose SIP for long-term goals of 5 years or more where higher returns over time matter more than short-term safety. Many financial planners recommend maintaining both an RD for emergency fund and short-term needs, and a SIP for long-term wealth building.

Final Thoughts

For the majority of salaried Indians, SIP is the right choice not because a lump sum is bad, but because SIP fits perfectly with how salaried income works. You receive money monthly, you invest monthly, and the automation ensures you stay consistent even when life gets busy or the market feels uncertain.

Start your first SIP today with whatever amount you can afford even ₹500 per month. Increase it every year as your salary grows. Add lump sum investments whenever you receive bonuses or extra income. And most importantly, stay invested through market ups and downs without panic-selling.

The salaried Indians who build serious wealth are not the ones who perfectly time the market they are the ones who stay invested the longest.

To begin investing, you will need a Demat and trading account. Read our step-by-step guide on how to open a Demat account in India to get started in under 30 minutes for free.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial advice. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully and consult a SEBI-registered financial advisor before making investment decisions.